Mutual Funds Simplified: A Complete Guide to Entry, Exit, Plans & Payout

Let’s get through the entry & exit plans in mutual fund, how they functions, things to remember while investing and lot more.

So, let’s take an example, imagine you’re going to watch a new movie. There's the ticket counter where you buy your ticket to get in, and then there are the doors you use to exit the theatre. But what if the movie theatre had a rule that if you leave before the intermission, they'd keep part of your ticket money? That's exactly how entry and exit fees work in mutual funds. This guide will walk you through the "gates" of your investment journey, from how you get in to how you can leave without any extra charge, ensuring you get the most out of your financial show.

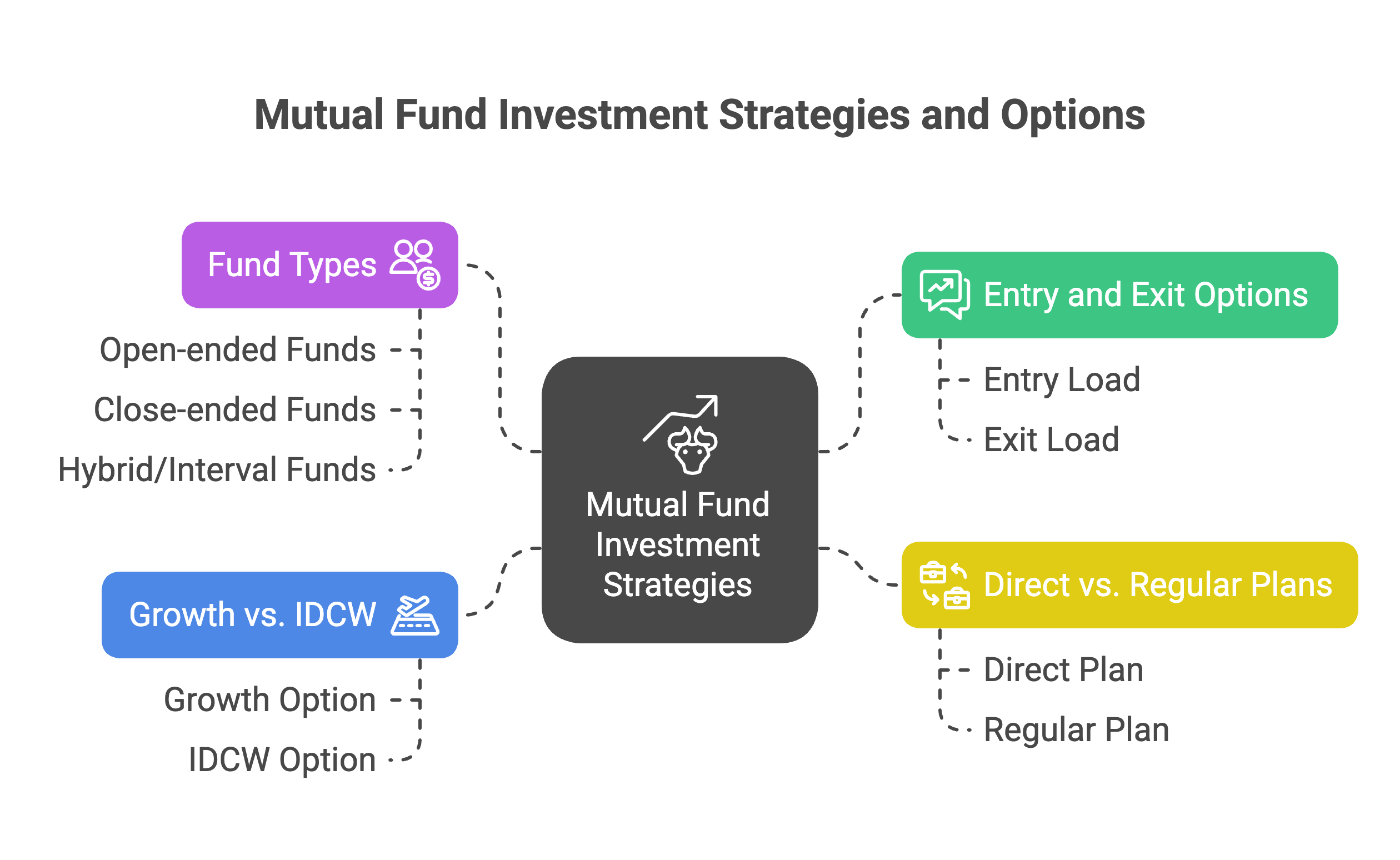

1. Entry and Exit Options

Think of a theme park ride. There’s always an entry gate where you get in and an exit gate where you leave. But some rides charge you extra if you leave midway! That’s how entry and exit loads in mutual funds work.

- Entry Load: A fee charged when you invest. In India, this is now mostly abolished.

- Exit Load: A fee charged if you leave (redeem) too soon. For example, you invest ₹1,00,000 in a fund with a 1% exit load if withdrawn within 1 year. If you redeem at 6 months, you get ₹99,000. If you redeem after 1 year, you get the full value with no charge. They are designed to stop you from leaving too early.

2. Open-ended, Close-ended, and Hybrid Funds

Imagine booking travel tickets. A bus pass (open-ended) lets you hop on or hop off whenever you want. A fixed train ticket (close-ended) only lets you travel at a set time and date. A tour package (hybrid/interval) lets you board or leave only at specific intervals. That’s exactly how mutual funds work.

- Open-ended Funds: Always open for sale and repurchase. They are flexible and liquid, with no end date. The number of units can go on rising as more investors buy into the scheme. The oldest open-ended scheme in India is the UTI, launched in 1986.

- Close-ended Funds: These have a window for investment (NFO) and a fixed maturity date. To provide liquidity, they are listed on a stock exchange. Fixed Maturity Plans (FMPs) are a type of close-ended debt fund that mimic a fixed deposit. However, FMPs have faced challenges and their popularity has waned from 25% of debt fund AUM in March 2014 to just 3% in March 2022.

- Hybrid/Interval Funds: A mix of both. They are open for entry and exit only at periodic, fixed intervals. A new version of an interval fund is the Target Maturity Fund (TMF), an open-ended passive debt fund with a stated maturity date.

3. Direct vs. Regular Plans

Imagine you want to buy a laptop. You can buy directly from the brand’s website (direct plan) or from a local dealer (regular plan).

- Direct Plan: Invest directly with the Asset Management Company (AMC). There is no distributor fee, resulting in a lower expense ratio and higher returns. A 1 percentage point difference in cost over thirty years means a difference of about 30% to your money.

- Regular Plan: Invest through a distributor or bank. They have a higher expense ratio due to the commission, which means slightly lower returns. This is a good option if you want guidance and portfolio maintenance services.

4. Growth vs. Income Distribution Capital Withdrawal (IDCW)

Think of apple trees. With the Growth option, you let apples stay on the tree, and the tree grows bigger, increasing in total value. With IDCW (called as Dividend), you pluck apples regularly and eat them.

- Growth Option: Profits are reinvested. The NAV grows due to compounding, which is best for long-term wealth creation.

- IDCW Option: Part of the profits are distributed as cash. The NAV falls after the payout. It’s best for those who want a regular income. The name was changed from "dividend" to IDCW on April 1, 2021, to clarify that the payout may also include a portion of your capital.

There are three kinds of IDCW:

- Payout: Cash is distributed directly to your bank account.

- Reinvestment: The distributed amount is used to buy more units. The net result is similar to the growth option.

- Transfer Plan: The IDCW amount is transferred to another fund. This is used to park profits in a more liquid product.

For most investors, the growth option is a better choice due to its compounding benefits and current tax advantages.

This blog comprises of all the main components of mutual funds, from the various fees you might encounter to the different investment plans available. You now understand the difference between open-ended and close-ended funds, as well as the benefits of choosing a direct plan over a regular plan. You've also learned about the two primary investment options: Growth and IDCW. With this knowledge, you are better prepared to navigate the world of mutual funds and make informed decisions for your financial future.

.png)

.png)

.png)

.png)

.png)